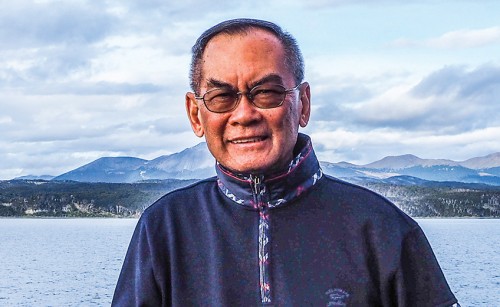

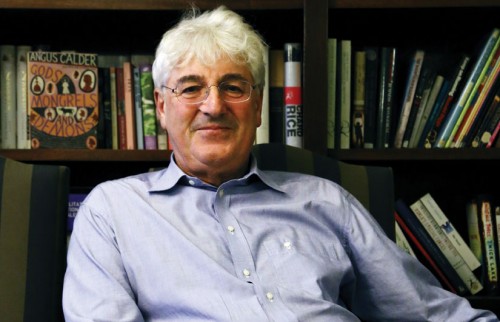

If not told that Kobsak Pootrakul, the baby-faced executive vice-president of Bangkok Bank, was an economist, we might judge from his descriptive eloquence that he was a man of letters. “If Thailand’s economy were a dam, it would be a dam that has run dry. If it were a car, it would be an old and ageing car that has run out of petrol.” It is a vivid prognosis that brings home the breadth and depth of Thailand’s grim economic situation. Mr Kobsak was giving a “Wisdom in Crisis” speech in August at the anniversary party for Elite+.

The economic growth rate remains at a halting 2%, the same as last year. China’s currency devaluation and sputtering stock market have driven the Stock Exchange of Thailand down for over a month. Exports have shrunk like a T-shirt after an overheated wash. Local consumption, which previously provided a cushion, no longer generates growth. Cash has evaporated for low-income earners such as farmers, while the middle-class are ridden with debt and overspending due to populist policies such as tax exemptions for first car and home purchases.

“High-end spending will not keep the economy rolling for long,” said Mr Kobsak. “In the end, the upper crust will feel the pain because lack of local consumption will eventually cripple overall businesses. “When the coup d’etat took place in May last year, many investors believed they would see a V-shape, a rebounding of economic activities as people came out to spend money after months of political protests, like it was after the 2010 red-shirt protests.”

Mr Kobsak was a member of the now defunct National Reform Council and Constitution Drafting Committee. As his work for those comes to an end, this rising star of the Thai economy can speak more freely about the Thai economy and his ideas for how to turn this ageing, sputtering jalopy into a powerful sports car. He asks people to be realistic and forget when Thailand’s growth rate was between 7 and 8%. “The dire economic situation will remain as it is for two or three years. What we need to do is not panic. We need to let cool heads prevail, and understand all the factors. Then we can make a sound decision that will carry us out of the crisis.”

The global economic downturn – especially ongoing problems with Greece’s debt and China’s currency devaluation – has had ramifications on Thailand’s business climate. But the most worrying aspect for Mr Kobsak is not the world economy, not low exports and local spending. The country’s economy is losing steam. For him, it resembles an “old and ageing company that has run out of new innovations and ideas to produce new products”.

“Thailand cannot create rising star industries like it once did,” he added. “In the late 1970s, we had the petrochemical industry, then we had automotive assembly. But what new rising industry do we have now?” Falling behind in innovation will cripple the country’s economy in the long term. One way to solve this structural problem is to find rising new sectors and help these through conducive and sustainable policies, including cash and knowledge and organized capacity building.

Mr Kobsak advises the broader public to be fiscally prudent. “Love your money and invest wisely. Understand the stocks you invest in and study the financial performance and nature of the company. Do not buy stocks just because marketers tell you to buy them.” There are always opportunities in crisis, Mr Kobsak insists. “It is time for businesses to try projects. Hotels might spin off into little boutiques, while ageing companies have time to learn about digital technology.

“The government should use this opportunity to develop infrastructure such as logistic projects and ready digital technology such as 4G concessions. It is a time to find new products and improve innovation. And do not focus too much on GDP. I would consider it a waste if the country can achieve more growth than a year before but fail to change our structural problems.”

{kind=link}

{kind=link}

{kind=link}